Petition To The President Of The Republic Of Liberia And Honorables Of The National Legislature On Violations Of Extant Laws And Regulations And Financial Irregularities By The Auditor General, Robert L. Kilby

1. We the Aggrieved and Concerned Employees of the General Auditing Commission (ACE) are pleased to bring to the attention of the President of the Republic of Liberia and Honorables of the National Legislature, reportable violations of extant laws and regulations and financial wrongdoings committed by the Auditor General, Robert L. Kilby, just within the period of three (3) months after assuming the position of Auditor General. The essence of this petition is to enable the President and honourables to determine on the basis of the dictates of Section 53.2, Executive Law of 1972, whether by the comportment exhibited by Mr. Kilby so far, he deserves to continue in office as Auditor General or otherwise. Section 53.2, Executive Law of 1972, stipulates that "there is hereby established in the Executive Branch of the Government an independent agency to be known as the General Auditing Office, which shall be headed by the Auditor General, who shall be assisted by at least two Deputies. The Auditor General and the Deputies shall be appointed by the President, by and with the advice and consent of the Senate. The Auditor General shall be appointed for a term of office of fifteen years and shall not be eligible for reappointment. The Auditor General shall be removed by the President for gross malfeasance or gross nonfeasance in office or for mental or physical disability or incompetence. In the absence of the Auditor General, the President shall appoint one of the Deputies to act in the capacity of Auditor General".

2. The Auditor General's post that Mr. Kilby holds is an eminent position and therefore Auditor General Kilby is required to be honorable in all his ways. Mr. Kilby’s comportment for the short time he has been in office is, to say the least, not honorable. This is because for the three months Mr. Kilby has been in office, we have observed several instances of violation of extant laws and regulations as well as abuse of public office and resources through impropriety by Mr. Robert Kilby. We have also observed the Auditor General’s lack of respect for the Public Procurement and Concession Act of 2005 and the Public Financial Management Regulations.

3. The ACE presents in this petition, evidence attesting to its foregoing assertions. The evidence is presented to the President and National Legislature, so as to enable them put an end to the demonstrable abuse of public office and resources as well as violations of extant laws and regulations by Mr. Kilby. The facts contained in this petition clearly show why the Mr. Kilby has severed more than 40 professional and trained staff of the GAC and also has singlehandedly been managing both the administrative and financial affairs of the Commission.

Financial Irregularities Committed by Mr. Kilby

Cell Phone Bought with GAC Money for Mr. Kilby’s Wife

4. The Auditor General and his newly hired Comptroller disbursed through a Payment Voucher with a face value of US$1,243.28 on October 17, 2012 from GAC Account to Cornelia Greene Mason, Mr. Kilby’s Executive Secretary. The payment, according to the voucher, was meant for the reimbursement for Iphones and accessories purchased by the Chief of AG Office Staff for the use in the Office of the Auditor General.

5. But contrary, we observed that the invoice and related documents accompanying the payment voucher indicated that the Iphones were rather purchased for Britney Marway Kilby (wife of Auditor General Kilby) in the United States of America from Apple Store Mall of Georgia, 3333, Buford Drive Suite Buford, GA, USA.

6. This expenditure is irregular, because there is no policy at the GAC that gives the Auditor General the right to use GAC funds to buy phone for his family or is his family entitled to phone at the expense of the GAC. Moreover, there is no budgetary allocation in the GAC budget for such transaction.

7. As a result, the Auditor General has violated Section 2218 of the Revenue Code of Liberia Act 2000 and therefore, it cannot stand as a charge to the GAC account. Section 2218 of the Revenue Code of Liberia Act 2000 provides that, no official or employee of government shall authorize or make any expenditure beyond the specific purpose set forth in any appropriation, allotment, and re-allotment or in excess of the amounts therein, and any such expenditure shall be void.

8. Therefore, full restitution of the money should be made into the GAC account by Mr. Kilby. Ref. Exhibit “A”

Bogus Audit Service Contract Entered with Parker and Associates

9. Procurement is an essential administrative and financial function and a process through which an entity obtains its optimal value for finances expended on goods, works and services. The effective and efficient use of financial resources in a competitive and transparent manner through a sound procurement process contributes to the achievement of the operational goals of both private and public entities. Efficient procurement practices generate savings on resources that would have been lost through improper procurement. Such savings make it possible for an entity to raise the amount of financial resources that could be utilized elsewhere, towards the attainment of the Entity’s objectives.

10. These views above appeared contrary to procurement practices pursued by Mr. Kilby at the GAC. In many of procurement activities and financial dealings conducted by him, they were not undertaken on a competitive and transparent manner. An instance of this is service contract awarded to Parker and Associates to audit GAC payroll. This service contract awarded did not meet the bidder’s qualification criteria as required by Section 32, PPC Act. Neither was the contract published as required under PPCA Schedule of Threshold, Section 1(b). The infraction observed denied assurance that services obtained from the contract, valued at US$27,000.00, were procured on the basis of lowest evaluated and most responsive bid, a requirement of Section 65(1), PPC Act.

11. Despite the fact that the service contract was awarded outside the jurisdiction of the PPCC Law, the contract was also awarded without the approval by the National Legislature, as required by Section (37.4) of the PFM Act. Section 37.4 of the PFM Act requires that notwithstanding the provisions of Section 37(3) above, the accounts of the General Auditing Commission shall be audited, at least once in every financial year, by a registered and reputable firm of qualified public accountants and auditors appointed by the legislature or possessing such other qualifications as the Legislature may deem appropriate, at such remuneration and on such other terms as the Legislature may determine. The remuneration of the auditor appointed under this session shall be defrayed from the funds of the General Auditing Commission.

12. The action on the part of the Auditor General undermines the authority of the Legislature that has the responsibility for authorizing the audit of the records and account of the General Auditing Commission.

13. It is thus suggested, that Mr. Kilby should be reprimanded by the Legislature for violating the dictates of the PPCC Law and PFM Regulations. Ref. Service Contract Exhibit “B”

Contract Value of US$105,300.00 awarded to V.I.P Security Guard to Manage the Auditor General Personal Security.

14. According to the Security Consultancy Agreement signed by Auditor General Kilby and Mr. Michael William, Chief Executive Officer of the Elite Security Guard Services The Auditor General has requested the V.I.P Security Guard to manage his (the Auditor General) personal security and to provide such other security to the GAC, as the Auditor General may require from time to time. The agreement further stipulates that the Auditor General employs and hires the Security Guard services on a non-exclusive basis to continue to manage his personal security and to provide security services and security protection for and on behalf of the Auditor General, its business and any other person (s) so designated by the Auditor General in writing for a period of 26 months. The security service is also required to investigate any matter of criminal nature and consequence.

15. The Ministry of Justice/Liberia National Police is responsible for the security and protection of people living within the borders of Liberia. Moreover, there is no budget line for security services, which is a violation of the Budget Law of 2012/2013. The justification provided by the Auditor General was clearly an attempt to siphon public funds and it cannot stand as a charge to the GAC account.

16. Moreover, the GAC has in its employ trained security personnel and LNP officers stationed at the GAC to provide security for personnel (including the Auditor General’s residence).

17. Furthermore, the dictates of the laws indicated in below were violated by Mr. Kilby in the award of the contract for the security services:

• Section 32, PPC Act (Pre-qualification of bidders procedures)

Violation: Pre-qualification of bidders procedures were not followed. This way, suppliers not meeting tax obligations etc could benefit from such contract awards.

• PPCA Schedule of Thresholds, Section 1(b) - Publication of contract awards

Violation: The contract for security services was not published. No other security services providers were considered and therefore the contract award cannot be said to be legitimate; value for money was therefore not derived.

• PPCA Schedule of Thresholds, Section 5 - Approval of contract awards by the Entity Procurement Committee.

Violation: There is no evidence that the Contract for the Security Services was approved by GAC Procurement Committee. Thus contract award is a violation of the PPC Act, and illegitimate. There was no sole source request from the Auditor General granted by the PPCC.

19. In addition to the above violations, Mr. Kilby has also violated the Budget Law of Liberia, which requires that activities/programs not budgeted shall not be undertaken unless request for supplementary budget has been sought and approved by the National Legislature.

18. Therefore, the awarding of the security service contract to a private security firm was a complete scheme employed by Auditor General Kilby to siphon funds from GAC. Ref. Exhibit C.

Questionable Transaction Involving Acquisition of Auditor General’s Vehicle

19. The Auditor General acquired a 2012 Expedition 4x4 King Ranch LHD Ford vehicle at the cost of US$56,000.00 at the expense of the meager resources of the GAC and in the face of “budgetary constraints”, as claimed by the Auditor-General.

20. The Auditor General personally took delivery of the vehicle on August 30, 2012. It is interesting to note however that the Auditor General, on August 31, 2012, wrote the Minister of Finance, Mr. Amara Konneh, requesting Duty Free Waiver for the purchase of said vehicle.

21. The transaction appeared to be fishy, because it is impossible to take delivery of the vehicle ahead of application and approval of Duty Free. Prestige Motor vehicles are bonded and can only be withdrawn from the bonded warehouse either by approved duty free by MOF or payment of duty. Therefore, to take delivery of vehicle before applying for Duty Free opens room for questions. The manner and form the transaction was conducted indicates that the vehicle was sold at duty paid price to the GAC and the duty waiver applied for by the Auditor General was an overpayment made to Prestige Motors, because GAC has already paid for the vehicle on duty paid price.

22. Without doubt, the duty waiver sought by the Auditor General though has not been granted by MoF, the implication means that GAC will retrieve the duty paid. We are yet to sight the duty in the books of GAC. The question requiring answer is how the vehicle was withdrawn on duty free from the bonded warehouse without approved duty free certificate from the MOF. Ref. Exhibit “D 1”

23. Though PPCC granted “no objection” on August 30, 2012, for the use of Restricted Bidding for the purchase of one for the incoming Auditor General, Auditor General Kilby on the same day, August 30, 2012 signed and took delivery of the vehicle, which is in direct violation of no objection granted by the PPCC. Ref. Exhibit “D 2”.

24. We also observed that Mr. Robert Kilby entered and signed a contract agreement with Prestige Motors on September 6, 2012; 6 days after he had taken delivery of the vehicle. This is irregular transactions, which is a violation of the PFM Regulation. See exhibit “D 3”.

25. This matter warrants thorough investigation by GAC Internal Audit Department to recover any overpayment made by GAC to Prestige Motors for the vehicle. Ref. Exhibit “E”.

GAC Payroll and Budget Constraints Issues

26. Salaries and allowances for personnel services are statutory provisions within the National Budget that no transfer by reduction can be made in the personnel services. For the GAC budget for 2012/2013, there was rather increment in the personnel services cost. This thus implies that the issue of budget constraint cannot hold for the almost 50 dismissed employees, because salaries and allowances for them were already appropriated by the Legislature in the GAC budget.

27. However, the fact of the matter is that the Auditor General was involved in extra budgetary expenditure by bringing along with him as the new Auditor General 19 additional staff with huge salaries ranging from US$3,000.00 to US$5,000.00. There were no budgetary allocations made for the additional staff hired by Mr. Kilby though GAC personnel service cost increased by a little over US$37,600.00, monthly. Such action by the Auditor General violates Section 2218 of the Revenue Code of Liberia Act, which provides that no official or employee of government shall authorize or make any expenditure beyond the specific purpose set forth in any appropriation, allotment, and re-allotment or in excess of the amounts therein, and any such expenditure shall be void.

28. It would have been prudent and lawful, if Auditor General Kilby has followed approved guidelines in seeking for extra budgetary approval from the Legislature before making the expenditure of the additional staff.

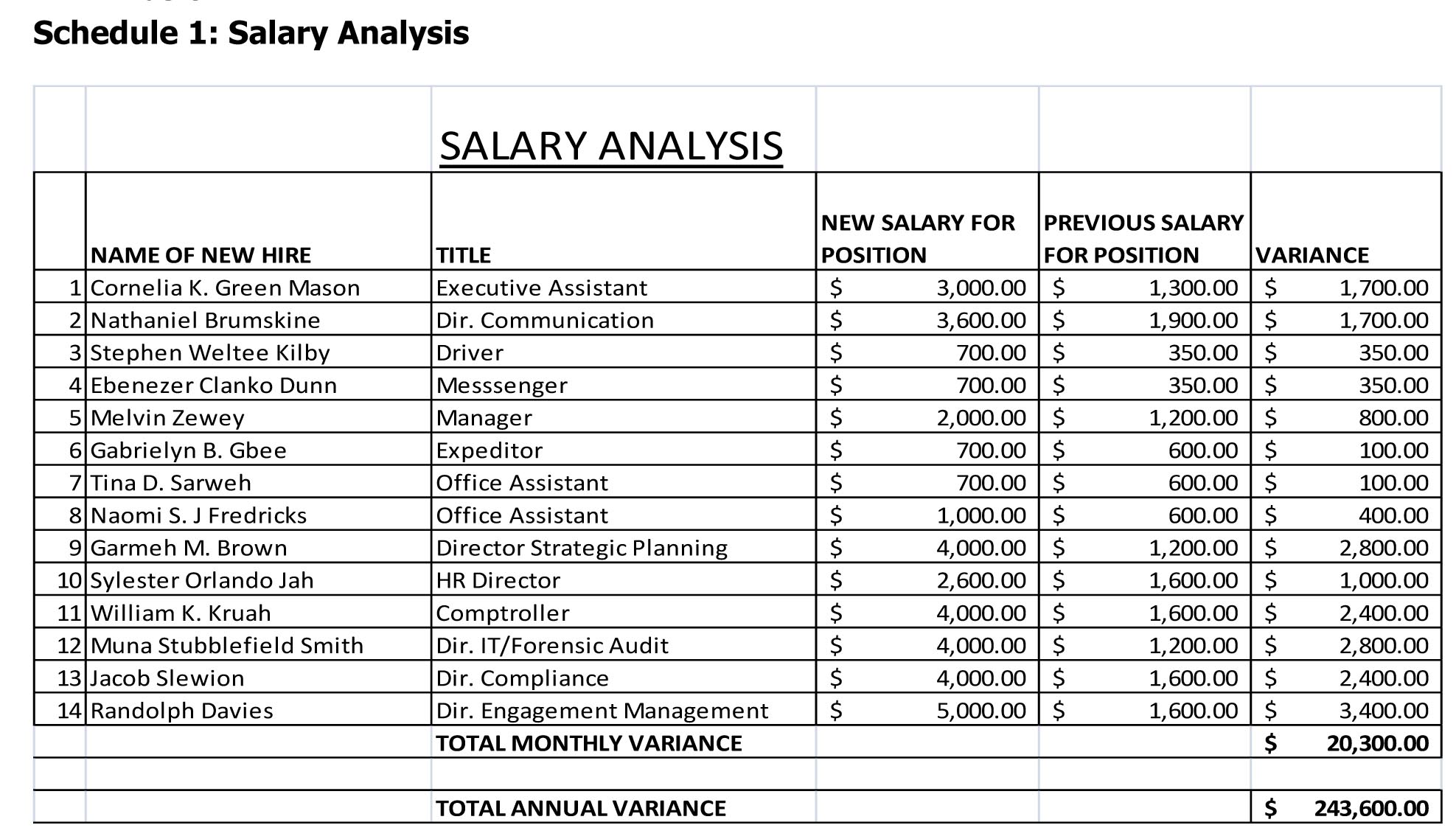

29. Mr. Kilby indicated in his dismissal letters to the almost 50 dismissed employees that the prevailing economic situation and its accompanying budgetary constraints has forced the GAC to initiate a cost-saving of the entire operation of the Commission, but failed to realize that he hired new staff and pay them more than the previous staff at the GAC. For instance, the existing Director of Revenue Audit is being paid US$1,600.00 per month, whilst the newly hired Director of IT Audit is paid US$5,000.00 per month. The total variance between the 14 old staff salaries and 14 new staff salaries is US$243,600.00 per annual. This is unrealistic and Robert Kilby is claiming budgetary constraints at the GAC. Ref. Exhibit “F” and Schedule 1 below.

|

30. Moreover, Mr. Kilby cannot justify his assertion that there are budgetary constraints, because he paid Muna Stubblefield Smith US$5,000.00 for the month of October 2012, when she started work at the GAC on October 25, 2012. This act does not only amount to payroll fraud but also runs contrary to GAC Human Resources Handbook and Civil Service Standing Orders, which require government employee to work for at least 10 days.

31. On October 25, 2012, the Auditor General wrote a memo with a Subject “Rumors Circulating within the GAC”, in which he indicated that “the GAC needs manpower to audit the 350 plus government and government entities disbursed around the country. Your services are needed to accomplish this objective”. He further indicated in the memo that he had no intention of selectively targeting audit trainees for termination of employment with the GAC. The Auditor General action of dismissing 43 persons from the GAC could been seen as contradictory to his own statements contained in the memo.

32. Given the fact that the Auditor General actions violates the Law and had no legal basis and coupled with the fact that the almost 50 dismissed persons had their salaries and allowances appropriated in the GAC budget for 2012/2013, the almost 50 dismissed staff should be immediately reinstated.

33. The payroll expenditure for the newly hired staff without budgetary appropriation made in the 2012/2013 cannot stand charged to the GAC account, unless the Auditor General obtain retrospective approval of the extra budgetary cost from the Legislature.

Violation of GAC Human Resource Policy

34. Section 8.2 of the GAC Human Resources Policy Handbook on position Elimination stipulates that: "in cases where restructuring of facilities and programs or budgetary constraints result in the layoff of GAC employees, reasonable effort will be made to provide advance notice to employees. If reorganization or lack of funding results in the elimination of the position to which an employee is assigned and if suitable alternative work cannot be offered by the GAC, the employee will receive as much notice as possible, but not less than 4 weeks. The GAC may at its discretion provide severance pay to employees who have been terminated for reasons beyond their control. In return for such severance the GAC will seek a routine release of liability".

35. As is apparent from the foregoing, none of the above provisions regarding redundancy was adhered to by the Auditor General. Notice was not given to the dismissed staff; no efforts were made to determine whether alternative positions existed for staff to be retrenched to be posted to Mr. Kilby thus exhibited absolute insensitivity in the dismissal of the almost 50 GAC staff.

36. Her Excellency, the President of the Republic of Liberia, and the Speaker, House of Representatives and the President Pro-tempo of the Liberian Senate, the above issues are symptomatic of others observed to be happening at the GAC. Because of their impact on the efficient and effective management of the GAC, we advise that their resolution be considered as a matter of urgency.

37. Furthermore, if Mr. Robert L. Kilby is not sanctioned by the Executive and the Lawmakers for his aberrant comportments, including dismissal and restitution of GAC funds misappropriated by him, it could send different signals to our stakeholders (i.e. the Liberian people and our international partners) that GAC is no longer the pillar of transparency and accountability and lacks integrity. Such perception would impact aid provided by Liberia's development partners.

38. We the Aggrieved Concerned Employees (redundant) of the GAC hereby affixed our signature to the above document for immediate action by the National Legislature and the President of the Republic of Liberia, Madam Ellen Johnson Sirleaf. Ref. Exhibit G.

Signed: __________________________

Sylvester K. Pewee

Attested: __________________________

Emmanuel T. Azango