Count The Liberian Banknotes And Reform Our Economy - PART I

By J. Yanqui Zaza

The Perspective

Atlanta, Georgia

November 21, 2019

|

Liberian Currency |

Has the President of the Republic of Liberia, Mr. George Weah addressed some of the discrepancies reported by the Kroll Investigating Team? The Kroll Investigating Team hired to audit the L$15B saga, as per the February 2019 report, stated that “…certain information provided by the CBL…contained inaccuracies and was incomplete…” Also, Kroll stated that it “…has identified discrepancies at every stage…such as “…the movement of funds within and out of the CBL’s vaults.” It recommended that the Liberian government should reform the managerial and its accounting system of the Central Bank of Liberia.

In my view, President Weah has performed the easy task by appointing Mr. Jolue Aloysius Tarlue as the Executive Governor-designate of the Central Bank of Liberia and constituted the Board of Directors of the Central Bank of Liberia. Additionally, he and the Liberian Lawmakers should institute measures to address the controversy of the banknotes, the rapid depreciation of our currency, and other budgetary issues.

Pertaining to the banknotes, Liberian officials state that the country should print L$35B banknotes because there is no money. Their statements are at variant with two different officials Reports of the Central Bank. Liberian currency in circulation was L$19B on December 31, 2018, according to page # 22 of the Audited Financial Statements of the Central Bank dated April 30, 2019.

Also, the second report of the Central Bank of Liberia (i.e., called Central Bank Annual Report) stated that Liberia had bank Liquidity of 38,956,700,000 and currency outside of the bank to be L$17,671,840,000. Yet, none of these figures in these two reports mean anything to the Liberian officials who insist that there is no money to pay employees. More so, how is it possible for the 2M of the L$500 banknotes to disappear between April of 2019 to October of 2019? Or what happened to the 26M L$100 banknotes and/or the 25M L$50 banknotes? Should we assume that poor residents were the depositors who withdrew the $19B from the commercial banks? I say no.

Count the Liberian currency: A good accounting system requires an entity (i.e., in this case, Liberia) to perform perpetual inventory (i.e., relying on bookkeeping entries, journal, ledger, balance sheet, etc.) and periodic system (i.e., a physical count of the inventory to determine the ending inventory). Therefore, the government should take a physical count of Liberia’s banknotes of L$19B in circulation since the perpetual method is giving questionable results.

This exercise should include obtaining identification of large withdrawals from the nine commercial banks since the completion of the April 30, 2019, external audit. It should be implemented, even if a new contractor prints L$5B, L$10B, L$22B or L$35B. This is because stabilizing Liberian currency is far beyond the issues of paying salaries. Liberia’s economic system should reassure our foreign suppliers and manufacturers that Liberia’s financial system is authentic and has adequate reserves to pay back loans borrowed by the government, commercial banks, or local entrepreneurs.

Add gold values to Liberia’s Net International Foreign Exchange Reserves: President Weah should write and request the Liberian Lawmakers to authorize an agency to mine gold from non-licensed goldfield/land and increase Liberia’s Net International Foreign Exchange Reserves. The adding of gold values to our Net International Foreign Exchange Reserves should calm the fear of foreign suppliers who are informed that the Central Bank does not have money to refund or repay debt owed by local merchants. It is true that foreign banks do not pay interest income on gold deposited at their banks. However, gold values, which price is to hit $1,650 in 2020, can be exchanged and/or sold for values, which could increase our country’s Net International Foreign Exchange Reserves, and by extension, reduce the prices of goods and services in Liberia.

Apply Generally Accepted Accounting Principles (ISA 16) and end selling government’s vehicles at book value and re-use them: Officials usually sell government’s vehicles after a few years in operation because the vehicles have reached its threshold (i.e., may be set at $500 or $10,000), over which it depreciates an assets. In any case, why should a government that does not use depreciation expense to reduce taxable income become involved in enforcing the rules of depreciation? Yes, besides tax benefit, depreciation rules help government officials to document the useful life of assets they need to perform. More so, unlike non-manufacturing country such as Liberia, countries sell government’s properties (i.e., computers, vehicles, machines, etc.) as a part of an economic benefit to entice and retain good-paying employers. So, Liberia should re-evaluate government’s vehicles and re-use them. Re-using vehicles would reduce our budgetary deficit, and by extension, reduce interest rates, and increase poor people’s purchasing power. What is the method? The government, relying on Generally Accepted Accounting Principles rules IAS 16, can re-evaluate government’s vehicles and re-use them.

Unearned revenue: The Liberian Revenue Authority, Central Bank of Liberia and others should prepare a schedule of reconciliation detailing earned income and unearned income, if not available. A schedule of reconciliation would help policymakers to understand that a portion of the government’s deposits at the Central Bank represents projected revenue for the previous fiscal period or subsequent fiscal period. This schedule is even important since the Central Bank reports on a calendar basis, while the government prepares its budget on fiscal year (July 1 through June 30).

I guess that a schedule of reconciliation would have provided information as to why the Central Bank reported that Liberia had a budgetary deficit of US $222M in 2018. Instead of providing clarity about the US $222M deficit, authorities took down 2018 Annual Report, which is contrary to Generally Accepted Accounting Principles-do not hide or takedown information, do not erase and/or delete numbers.

Schedule with the explanation of budgetary numbers: It is true that “number cannot lie,” as per the old adage. However, preparers might inflate numbers, underreport numbers, or misclassify numbers, causing readers and policymakers to make wrong decisions. The government ministries, agencies and all institutions involved in generating numbers should provide accurate and reliable numbers. The Finance Ministry should prepare a schedule and explain why Liberia’s revenue projections indicate that the country is not facing financial crisis.

For instance, after the deadly Ebola crisis, the government reported that the crisis affected our revenue. Yet, the Ministry of Finance projected US $442 for 2013/2014 and US $484M 2014/2015 after the Ebola years, amounts far higher than US $342M in 2011/2012 and US $392M in 2012/2013. Our revenue numbers did not reflect weak economic activity, rather the numbers implied that our economy was strong in 2013/2014 (i.e., Ebola years) as well as in 2014/2015 (i.e., post-Ebola year).

Fast forward to 2018. President Weah’s economic advisers stated that the country was broke and income-generating activities were not doing well. They also stated that prices for major exports were down and many local companies (oil palm, etc.) were slowing down their economic activities such as laying off tax-paying employees. Again, the Finance Ministry has projected revenue numbers that indicate that our economy is strong. In 2018/2019, the revenue projection was US $562M; US $511M in 2019/2020; and US $528M in 202/2021.

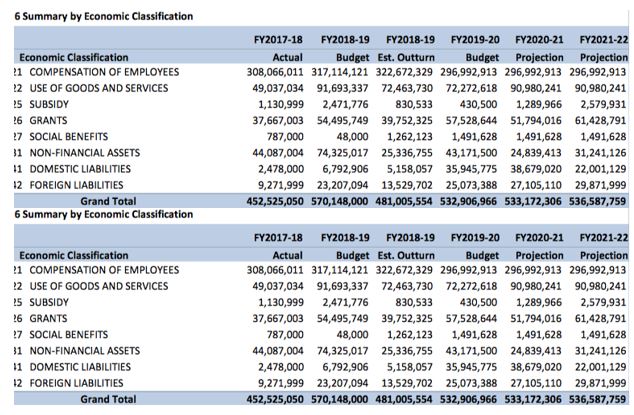

As per the schedule below, the wage bills projections did not indicate that our economy was weak. For instance, none of the projections included salary harmonization because the amount allocated for the wage bills did not significantly change in 2018/2019, 2019/2020 and 2020/2021.

President Weah and his economic advisers should begin to do the right thing, and everything else will be manageable.

Part II next.

(http://www.cbl.org.lr/doc/Annual_Report_2018_Feb_12_2019.pdf)

Central Bank 2018 Annual Report

(https://www.cbl.org.lr/doc/FinancialStatement_2018.pdf)

Central Bank 2018 audited Financial Statements.

|

|---|